Last week my husband and I sat down with an adviser to begin the paperwork for his retirement. This feels like the second scariest decision we've ever made during our marriage. The first was when we decided to live on one income so that I could be at home with our children.

Retirement sounds wonderful: no more worrying about the hassle of daily work schedules, the trepidation of driving to work in blizzards, and the insanity of workplace politics.

But with that comes living on a fixed income. Three years ago the prospect of living on a retirement income didn't seem like such a big deal (at least from my perspective). But last year our property tax took a 40% leap and the county assessor says we can expect 5-10% increases annually for the foreseeable future. I have to wonder now how long before property tax will price us out of our house.

Then inflation hit us like a bulldozer, and suddenly, property tax is only a tiny fraction of our concerns. Blindsided by all this economic upheaval, my husband has put off retirement for a while, hoping our country's financial earthquakes will soon settle into a more stable landscape.

But it looks like inflation is here for a while and we have to decide if we're up to the challenge of making ends meet. Answer: Yes. Maybe? We hope so.

No reason to worry, right? Of course, millions of others before us have taken this plunge into retirement. And really, even those earning regular paychecks are struggling since for many, wages have not kept up with inflation, especially in the last year or two.

The truth is, financial instability has been a fixture in our society for quite some time. Four years ago I wrote this on my blog:

Four years ago, when inflation was outpacing income by 9% over a 13 year period, I began to focus my writing on different ways one could get by on less. Today we need this help even more.

Real Inflation

The UN Food and Agriculture Organization (FAO) reports that between November 2020 and November 2021, food prices worldwide increased 31%. In just one year! Federal economists and news agencies are not reporting this kind of inflation but we don't need the news to tell us prices are going up. We see it every week as we tally up the grocery bills.

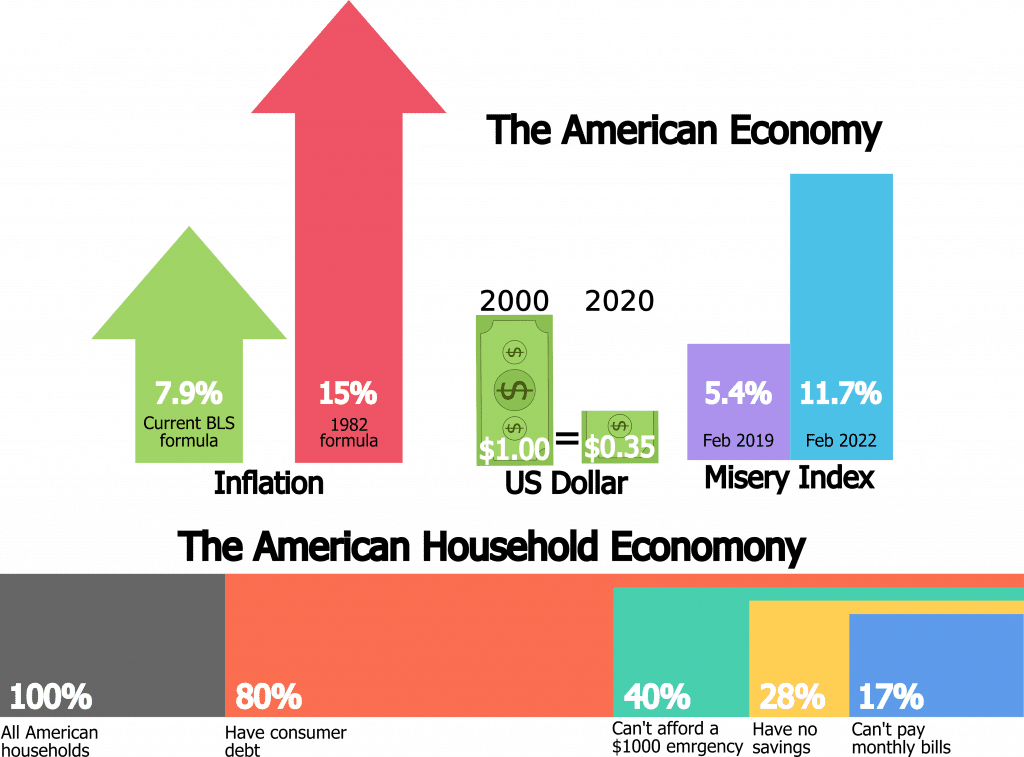

The Consumer Price Index (CPI) is the principle indicator of inflation that the US Bureau of Labor Statistics (BLS) uses. The BLS has been tracking the CPI since 1919. But the way it is calculated today is much different than it was in 1919 and in the last 40 years there've been even more changes to the formula for calculating inflation.

Back in the 70's, rampant inflation made President Carter unpopular. That's when economists came up with the term “misery index,” a combination of inflation and unemployment. Then BLS changed the formula for calculating inflation, from “cost of goods” to “standard of living.” The formula has been changed several times since then. For example, prior to President Reagan the CPI included things like food and fuel. The result of these changes to the formula is almost always an inflation rate that is lower than what consumers and investors actually experience.

Last December BLS reported a 7.9% inflation rate over December 2020. “The highest inflation since 1982!” the headlines said. But that's only a fraction of the story. According to US economist John Williams, if the CPI today were to be calculated the way it was before the Reagan era, inflation would be 15%, double what's being reported today.

What about wages?

Don't wages go up along with inflation? Not necessarily. There's always a lag between price increases and wage increases. Today the difference between wages and prices is even more acute. According to the Conference Board, a professional organization for public and private corporations, wages are going up right now about 3%. That means that prices are going up five times faster than wages.

What this all means is that, fixed income or not, it's getting harder and harder for everyone to make ends meet. Government leaders assure us this inflation will be short lived. Maybe they're right, but how long can your family stay afloat with this kind of financial trend?

Making ends meet is always important, but now you'll need a whole new set of skills to do it. So I will be writing columns on how one can survive — maybe even thrive? — despite all this economic uncertainty. I'm not a financial adviser, by any stretch of the imagination. I can't tell you the best place to invest your money. But, having lived on a single income for close to 30 years, I do know a bit about how to live on less and make your money go further.

Stick with me, and we'll find ways to make our money go further and ride out this tide of economic uncertainty.